The Mathematics of Filling Tax Brackets

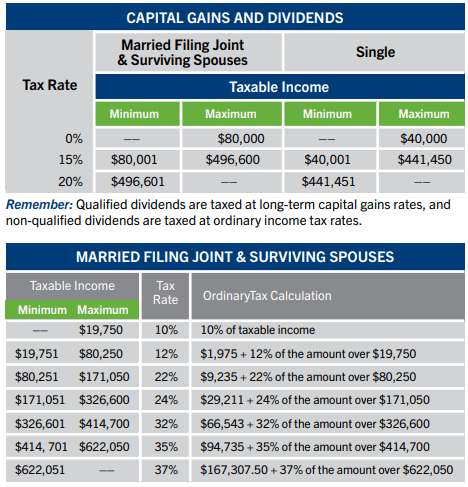

Chuck and Debbie both recently retired at the age of 65. They estimate their 2020 income will be $55,000 (including $10,000 of qualified dividends). They will take the standard deduction when filing their 2020 federal tax return. In 2020, the standard deduction for married couples who are both age 65 and older is $27,400.

FULLY UTILIZE THE 0% CAPITAL GAINS BRACKET

If Chuck and Debbie want to fully utilize the 0% capital gains bracket, they must first calculate taxable income by subtracting the standard deduction ($27,400) from their total income ($55,000). Based on this calculation, Chuck and Debbie’s taxable income is $27,600.

In order to determine the amount of long-term capital gains they can realize without paying additional income tax, Chuck and Debbie must subtract their taxable income ($27,600) from the maximum 0% capital gains threshold ($80,000). Based on this calculation, Chuck and Debbie can realize $52,400 of long-term capital gains without paying additional income tax.

When determining how much room remains in the 0% capital gains bracket, keep in mind that ordinary income is counted first, with long-term capital gains and qualified dividends stacked on top. For example, if a married couple has $70,000 of ordinary taxable income plus $20,000 of long-term capital gains and qualified dividends, the $70,000 of ordinary income is counted first. Consequently, only half of the couple’s longterm capital gains and qualified dividends fall into the 0% capital gains bracket. The remaining half is taxed at 15%.

IMPLEMENT STRATEGIC ROTH CONVERSIONS

Instead of realizing additional long-term capital gains, Chuck and Debbie decide they would rather convert a portion of their traditional IRA assets to a Roth IRA. They hope to utilize the 12% ordinary income tax bracket without moving any of their $10,000 of qualified dividends into the 15% capital gains bracket.

Chuck and Debbie’s total taxable income (including the Roth conversion) must not exceed $80,000 if they want to avoid having their qualified dividends taxed at the 15% capital gains rate. Accordingly, in order to determine the amount of traditional IRA assets to convert to a Roth IRA, Chuck and Debbie must subtract their taxable income ($27,600) from$80,000. Based on this calculation, the couple can convert $52,400 from a traditional IRA to a Roth IRA without exceeding the 12% ordinary income tax rate or the 0% capital gains rate.

If Chuck and Debbie instead choose to convert $52,650 to a Roth IRA, their taxable income would total $80,250 (the top of the 12% ordinary income tax bracket). However, because capital gains stack on top of ordinary income, $250 of qualified dividend income would be pushed into the 15% capital gains bracket.

While there are many advantages to fully utilizing lower tax brackets, taking additional taxable income can have negative consequences in certain situations. For example, doing so may lead to an increase in the taxability of Social Security retirement benefits or higher monthly Medicare premiums. Before implementing either of the strategies discussed above, you should speak with a tax professional.

The IIAR and ARF reserve investment funds are currently managed by Stifel Financial Services under the investment policy established by their respective board of directors.